Introduction

In the years leading up to retirement, your focus will probably shift away from the day-to-day financial matters, such as paying off the mortgage, to thinking about your retirement. How much money will you need? Have you been contributing enough to super and how can you increase your super balance to fund a comfortable retirement? It’s important to consider that your retirement may last a long time. Increases in life expectancy mean that you may live for 20 or even 30 years after you retire around age 65. You may want to start working less and consider moving to part-time employment. You may also start thinking about ways to provide financial assistance to your children once you are gone.

Careful planning before you retire can make a big difference to your superannuation balance, making it last longer and giving you peace of mind that your hard-earned wealth is protected.

Major financial decisions

- Planning what you want to do in retirement

- Accumulating enough wealth to enjoy a comfortable retirement

- Moving to part-time work

- Providing for your children

How we can help

- Budgeting and goal setting

- Debt management

- Investment strategies

- Insurance

- Superannuation planning

- Estate planning

Accessing Your Superannuation

How can you boost your salary and pay less tax?

Non-commutable allocated pensions (NCAPs) allow you to access your preserved superannuation without having to retire. If you are over 55, but less than 65 years of age, you have the option to start an NCAP. This enables you to:

- gradually reduce your work hours without reducing your take-home income

- boost your retirement savings by contributing to super through salary sacrifice, and

- pay less tax on income and super earnings.

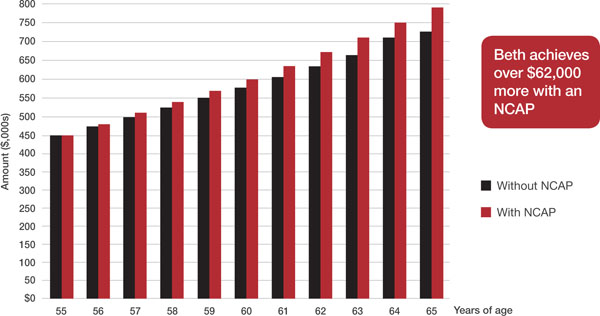

Beth’s story

Beth, aged 55, works as an IT consultant and earns $110,000 a year. She enjoys her job and hopes to retire from full-time work when she reaches 65. Her current superannuation balance is $450,000.

By beginning an NCAP, Beth can supplement her income using her current superannuation fund, while sacrificing a substantial pre-tax amount of her income into superannuation.

NOTE: No change in take-home pay before/after strategy. No change in risk profile. Estimated investment return is 5.8% pa (super – balanced), 7% pa (pension – balanced), super contribution remains at 9%. 2010/11 income tax rates used. Past performance is not a guarantee or an indication of future performance.

- 60+pay no tax on your superannuation benefits, unless you’re a long-term public servant

- 70%of Australian retirees rely on the pension as their principal source of income